As I write this on Sunday night, the Brent oil price is around $109, a huge 18 percent jump from Friday. Markets were slow to price the enormity of what was happening a week ago, but at this point Brent is up 50 percent from before hostilities broke out. At times like this, it’s tempting to think this spike can go a lot further, but I think there’s a number of reasons to be cautious and – if anything – to consider catalysts that might make the oil price fall. That’s what I do in this post. The most obvious catalyst is that oil tankers start running again. Even just a few have the potential to change market psychology given the massive risk premium that’s now being priced.

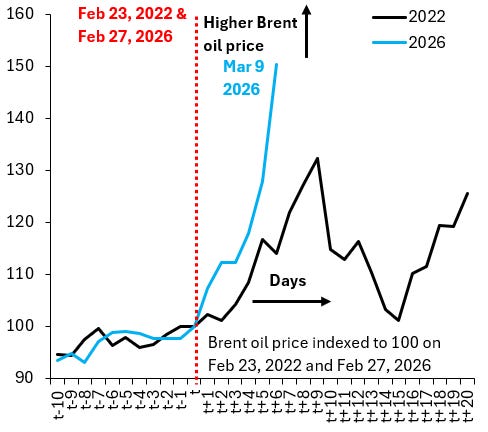

The chart above is one my readers will by now be familiar with. It compares – in event time – the current oil shock to the one after Russia invaded Ukraine. I index the Brent oil price to 100 on Mar. 23, 2022 (the day before the invasion) and on Feb. 27, 2026 (the day before the current episode started). The cumulative rise in Brent is now 50 percent versus a peak of 32 percent – on a similar time scale – back in 2022. After a great deal of complacency a week ago, markets have now realized the enormity of this shock and are pricing it accordingly. If anything, we’ve now reached a point where markets are in outright panic and so it’s worth thinking about catalysts for oil prices to fall. I can think of three such catalysts:

-

The Strait of Hormuz closure is “old news:” the Strait of Hormuz has now been closed for around a week. I’m the first to admit that markets were slow to price the enormity of this. Indeed, one week ago I was banging the drum that Brent needed to rise further. But at this point the cat’s out of the bag. The Strait can’t get any more closed than it already is, so we’re really just talking about whether the current level of Brent correctly prices this supply disruption. That’s super tricky, which is basically what my next two points are about.

-

The Strait of Hormuz can only get more open from here: there’s only one way things can go from here, which is that tanker traffic through the Strait resumes. The only uncertainty is how quickly this happens and in what size. My best guess is that – given the large risk premium that’s now priced in Brent – even a small number of oil tankers will be enough to change market psychology. If the US Navy successfully thwarts drone attack on these ships, all the better.

-

Iran’s regime falls: it’s not that long ago that there were massive protests on the streets of Tehran, which were put down with extreme violence. With every day that aerial bombardment continues, the regime’s grip on power weakens. I have no insight on how far we are from a tipping point – maybe it won’t come – but the probability that the regime falls is as high as it’s ever been and rising.

The closure of the Strait of Hormuz is old news at this point. So what’s happening is entirely psychological. Markets are weighing the current closure against how quickly oil tanker traffic can restart and on what scale. That’s the kind of thing that can change on a dime.